This month, I sold some counters to raise cash for more compelling ideas. Also, increase my stakes in a few of my US counters.

(figure in bracket represents the % the counter is occupying my portfolio based on cost)

Sold

1. Divested ISEC completely at $0.315 even though it has reported a good set of numbers in the latest quarter. Still find this an interesting outfit but decided to temporarily say goodbye to it as I wanted to buy other counters.

2. Sold Hock Lian Seng (2.0%) at $0.47 for a gain of 7.6%. This reduced my stake in the company and it now only occupies only 2% of my portfolio. Continue to believe in its ability to sustain its dividend based on the cash that it has and its strong order book. However, I relatively like my new positions.

Accumulate

1. Re-entered Capital Mall Trust (2.3%) at $2.02 after attending a sharing by Deputy CEO of Capital Mall Asia, Wilson Tan. Basically, he opined that retail mall is here to stay and Capital Mall will continue to be a powerhouse a decade later. With the purchase of CMT, I now own a slew of retail REITs but each for a different reason.

SG Reit - my longest holding for its focus on mall in prime area and its overseas exposure.

FCT - for its focus on sub-urban malls with most of them near MRT stations.

CMT - for not resting on its laurels and continues to take actions to be at the fore-front of retail mall.

2. Added more UMS (4.1%) at $1.05 after it announced a good set of Q3 results. Optimistic about its upcoming performance for the next few quarters and confident that it will at least maintain its dividend.

3. Added Intuitive Surgical (1.1%) @388.85 as I forgot to update my spreadsheet for its stock split! Luckily, bought only 4 shares to round up my total shares to 10. Let's hope it can continue with its splendid growth, then the mistake can become a blessing in disguise.

4. Added Vail Resorts (0.7%) @235.77 as it continues to report good growth from its acquisition. While management guided that 2018 growth might be slower due to the strong growth this year, long term prospect should remain good.

5. Re-entered Priceline (1.0%) @1655.75. I had sold earlier in September at 1840.6, making a loss of 5.1%. Since then the group announces a solid Q3 results which beats its own guidance. However, the market bashed it down due to another muted Q4 guidance. Seeing that Priceline always beats its own estimate, I decided to re-enter Priceline at a better price.

Showing posts with label ums. Show all posts

Showing posts with label ums. Show all posts

Tuesday, 28 November 2017

Thursday, 26 October 2017

A look at my recent buys (Part 2) - Hock Lian Seng vs UMS

Hock Leng Seng (HLS) vs UMS? Why compare them? How are they related?

Nothing except that both are listed on Singapore Exchange and I bought them recently in September as dividend counters.

What do they do?

Hock Lian Seng is a leading civil engineering group that is established for 45 years. It is listed on SGX mainboard in December 2009. At any one period, the group does not have many projects but they have big projects with revenue that is recognized over a few years. Some recent completed projects include Marina Bay Station, Marina Coastal Expressway. On-going projects include CAG airport runway and Maxell Station. Upon listed, they forayed into property development and had developed industry building such as ARK@Gambas and ARK@KB and collaborated to developed the Skywoods condominium. The remaining project that the group is doing now is Shine@Tuas South. The other segment is investment properties which contributed negligibly in the latest financial year.

As seen from the segment value, the group seems to have gone a full circle with tapering civil engineering projects to an increase in it after a few years in experimenting properties development and investment. Going forward, it seems that they will be focusing on civil engineering business.

UMS is a is a one-stop strategic integration partner providing equipment manufacturing and engineering services to Original Equipment Manufacturers of semiconductors and related products. It is formed with the merger of Norelco Centreline (listed on SESDAQ in 2001 and upgraded to mainboard in 2003) with UMS Semiconductor in 2004. The key change in their product occurred in 2010/2011 when they acquired Integrated Manufacturing Technologies Pte Ltd and Integrated Manufacturing Technologies Inc. Since then, their revenue is mainly from Applied Materials.

Recent development, results and price movement

Hock Lian Seng proposed a special dividend of 10 cents in the latest financial year. Wow, a big windfall for investors who have invested in the company before that. Unfortunately, I am not one of them. 20171H performance has been muted as there is no contribution from property development. Revenue from Civil Engineering segment was flat from previous year. The bright spot since the beginning of the year is the record order book which stands at a high of 890 million. Also, it has about 27 cents of cash per share which means I am just paying about 18 cents for its solid order book. Share had drifted to $0.4+ in August/September when I made my purchase. It was moving up over the past week and is now at $0.51.

UMS renewed its integrated system contract with Applied Material for 3 years (and has the option of extending it for another 3 years). It is also attempting to diversify its customer base by subscribing to 51% of the enlarged share capital of Kalf. Recently, it has also gone XB for its 1-for-4 bonus. Its price has dropped from its high of $1.2+ (pre-bonus) in May/June to $0.9 (pre-bonus) when I made my purchase. It has gone ballistic after XB recently and is now at $0.99 (post-bonus).

Dividend and Sustainability?

Year HLS UMS

2016 12.5 c 4.8 c (adj)

2015 2.5 c 4.8 c (adj)

2014 4.0 c 4.2 c (adj)

2013 1.8 c 3.8 c (adj)

2012 1.8 c 3.8 c (adj)

As seen from the above table, both companies have been quite consistent in giving out dividends with HLS giving out special dividend periodically and UMS has increased its dividend.

Dividend payout for HLS around mid 30%, while UMS ranges from 70+% to 100+% if based on net profit. Based on free cash flow, UMS is around low 80%. Also, as mentioned earlier, HLS has about 27 cents in cash; while UMS cash holding is around 14 cents.

Based on the above, I am quite confident that both companies will sustain their pay out in the coming year (HLS – 2.5c, UMS – 6c) and this will translate to a yield of about 4.9% for HLS and 6.1% for UMS.

Conclusion

I first purchased both when their price has slid downwards in August/September. I was quite impressed by Hock Leng Seng as it has a strong net profit margin and return of equity. The property development has probably masked the NPM and ROE figures and I have not spent time drilling down on its AR. However, if I based it on 2009, 2010 figures when property development has not started NPM is around 10% and ROE is high 20%. Impressive numbers.

Based on these numbers, order book and cash per share, I have added slightly more this month, bringing my average price to $0.45. I would like to see how things unfold in the coming quarters before deciding if I would accumulate more.

With the contract renewal, there is more certainty of UMS for at least the next few years. I have not added to UMS since my purchase at an average price of $0.76 (adj) in August, as the price has ran up and I was waiting to see if it would correct to below $0.80 after XB. The run up after XB was totally unexpected. I would be waiting for its Q3 results and the price then before making further decision.

Nothing except that both are listed on Singapore Exchange and I bought them recently in September as dividend counters.

What do they do?

Hock Lian Seng is a leading civil engineering group that is established for 45 years. It is listed on SGX mainboard in December 2009. At any one period, the group does not have many projects but they have big projects with revenue that is recognized over a few years. Some recent completed projects include Marina Bay Station, Marina Coastal Expressway. On-going projects include CAG airport runway and Maxell Station. Upon listed, they forayed into property development and had developed industry building such as ARK@Gambas and ARK@KB and collaborated to developed the Skywoods condominium. The remaining project that the group is doing now is Shine@Tuas South. The other segment is investment properties which contributed negligibly in the latest financial year.

As seen from the segment value, the group seems to have gone a full circle with tapering civil engineering projects to an increase in it after a few years in experimenting properties development and investment. Going forward, it seems that they will be focusing on civil engineering business.

UMS is a is a one-stop strategic integration partner providing equipment manufacturing and engineering services to Original Equipment Manufacturers of semiconductors and related products. It is formed with the merger of Norelco Centreline (listed on SESDAQ in 2001 and upgraded to mainboard in 2003) with UMS Semiconductor in 2004. The key change in their product occurred in 2010/2011 when they acquired Integrated Manufacturing Technologies Pte Ltd and Integrated Manufacturing Technologies Inc. Since then, their revenue is mainly from Applied Materials.

Recent development, results and price movement

Hock Lian Seng proposed a special dividend of 10 cents in the latest financial year. Wow, a big windfall for investors who have invested in the company before that. Unfortunately, I am not one of them. 20171H performance has been muted as there is no contribution from property development. Revenue from Civil Engineering segment was flat from previous year. The bright spot since the beginning of the year is the record order book which stands at a high of 890 million. Also, it has about 27 cents of cash per share which means I am just paying about 18 cents for its solid order book. Share had drifted to $0.4+ in August/September when I made my purchase. It was moving up over the past week and is now at $0.51.

UMS renewed its integrated system contract with Applied Material for 3 years (and has the option of extending it for another 3 years). It is also attempting to diversify its customer base by subscribing to 51% of the enlarged share capital of Kalf. Recently, it has also gone XB for its 1-for-4 bonus. Its price has dropped from its high of $1.2+ (pre-bonus) in May/June to $0.9 (pre-bonus) when I made my purchase. It has gone ballistic after XB recently and is now at $0.99 (post-bonus).

Dividend and Sustainability?

Year HLS UMS

2016 12.5 c 4.8 c (adj)

2015 2.5 c 4.8 c (adj)

2014 4.0 c 4.2 c (adj)

2013 1.8 c 3.8 c (adj)

2012 1.8 c 3.8 c (adj)

As seen from the above table, both companies have been quite consistent in giving out dividends with HLS giving out special dividend periodically and UMS has increased its dividend.

Dividend payout for HLS around mid 30%, while UMS ranges from 70+% to 100+% if based on net profit. Based on free cash flow, UMS is around low 80%. Also, as mentioned earlier, HLS has about 27 cents in cash; while UMS cash holding is around 14 cents.

Based on the above, I am quite confident that both companies will sustain their pay out in the coming year (HLS – 2.5c, UMS – 6c) and this will translate to a yield of about 4.9% for HLS and 6.1% for UMS.

Conclusion

I first purchased both when their price has slid downwards in August/September. I was quite impressed by Hock Leng Seng as it has a strong net profit margin and return of equity. The property development has probably masked the NPM and ROE figures and I have not spent time drilling down on its AR. However, if I based it on 2009, 2010 figures when property development has not started NPM is around 10% and ROE is high 20%. Impressive numbers.

Based on these numbers, order book and cash per share, I have added slightly more this month, bringing my average price to $0.45. I would like to see how things unfold in the coming quarters before deciding if I would accumulate more.

With the contract renewal, there is more certainty of UMS for at least the next few years. I have not added to UMS since my purchase at an average price of $0.76 (adj) in August, as the price has ran up and I was waiting to see if it would correct to below $0.80 after XB. The run up after XB was totally unexpected. I would be waiting for its Q3 results and the price then before making further decision.

Saturday, 7 October 2017

A closer look at my recent buys (Part 1) - iFAST

In August and early September, I have initiated positions on iFAST, Hock Lian Seng, UMS and 800 Super (re-entered) after chancing upon their price drop of about 20% from recent high in June. I did a quick scan on their news and did not find any major fundamental change in their business and hence took a bite.

I decided to take a closer look at the them to decide if I should add more to my initial holdings. I will start with iFAST as I am most excited about it after scanning through their latest annual reports.

What do they do?

Listed on SGX on 11 December 2014, iFAST business revolves around internet-based investment products distribution platform with assets-under-administration (AUA) of about 6.1 billions. It has presence in Singapore, Malaysia, Hong Kong and China. Two main business divisions, business-to-business (B2B) and business-to-consumer (B2C) with B2B contributing 75% of revenue in 2016. About 83% of its net revenue is recurring.

Recent development, results and price movement

iFAST has a strong rebound in their 20171H results. Revenue was up by about 20% and net profit up by 75% but this came from a weak 20161H results. The poor results in 2016, a 55% drop in EPS has caused the share price to plunge from $1.35 to $0.85 for that year. The price continued to slide in 2017 till April to reach a low $0.60. The release of its strong results this year has resulted in a strong rebound of its share price, reaching a high of $1.1+ in June.

It has also launched its SGX stockbroking service in June 2017 after being admitted as a Trading Member of Singapore Exchange Securities Trading Limited (“SGX-ST”) and a Clearing Member of The Central Depository (Pte) Limited (“CDP”).

Management

Based on what I read on the annual reports and action taken by the company, I think iFAST Chairman, CEO and co-founder Lim Chung Chun is a forward looking and strong leader who drives the company to put their company values (Integrity, Innovation and Transparency) into action. The following is the final paragraph from 2016 report.

With the exception of 2016, iFAST has grown both its top and bottom lines, with its EPS growth outpacing its net revenue growth.

Base on the above data, I believe the company should be able to continue to grow its earning at a rate of 20% to 30% for the next few years.

Valuation

Together with the rest of the market, iFAST's price has rebounded quite a bit since the beginning of October and closed at $0.96 on 6 October. Forward PE based on the current price and projected EPS is about 26x. Assuming I am right about its ability to grow at 20% to 30% in the next few years, forward PEG ranges from 1.1 to 1.3. My personal take is that it is fairly priced with potential to surprise on the up side but risk still lingers.

When will I sell?

These four rules still apply.

Conclusion

My first encounter with the company was more than a decade ago when I opened my Fundsupermart account. Did not really use its services as I was on dollardex then. Recently, I wanted to explore its FSMone platform for stock trading and hence decided to register an account. Apparently my record is still in their data base and I need to re-activate my account which I will probably do by the end of the year.

As an investing idea, I came across it somewhere in late 2015 but the PE was crazy then. The sell down due to poor results in 2016 and the recent correction provides me an opportunity to buy a small stake in the company.

I can sense my excitement as I read the development of iFAST over the years and imagine what more can come from them in years to come. Hence, I decided to buy more yesterday at a price of $0.975 (yes, I am not good at market timing). Together with my initial purchases, my average price is $0.93.

I am prepared to add more to this counter at the appropriate junctures.

I decided to take a closer look at the them to decide if I should add more to my initial holdings. I will start with iFAST as I am most excited about it after scanning through their latest annual reports.

What do they do?

Listed on SGX on 11 December 2014, iFAST business revolves around internet-based investment products distribution platform with assets-under-administration (AUA) of about 6.1 billions. It has presence in Singapore, Malaysia, Hong Kong and China. Two main business divisions, business-to-business (B2B) and business-to-consumer (B2C) with B2B contributing 75% of revenue in 2016. About 83% of its net revenue is recurring.

Recent development, results and price movement

iFAST has a strong rebound in their 20171H results. Revenue was up by about 20% and net profit up by 75% but this came from a weak 20161H results. The poor results in 2016, a 55% drop in EPS has caused the share price to plunge from $1.35 to $0.85 for that year. The price continued to slide in 2017 till April to reach a low $0.60. The release of its strong results this year has resulted in a strong rebound of its share price, reaching a high of $1.1+ in June.

It has also launched its SGX stockbroking service in June 2017 after being admitted as a Trading Member of Singapore Exchange Securities Trading Limited (“SGX-ST”) and a Clearing Member of The Central Depository (Pte) Limited (“CDP”).

Management

Based on what I read on the annual reports and action taken by the company, I think iFAST Chairman, CEO and co-founder Lim Chung Chun is a forward looking and strong leader who drives the company to put their company values (Integrity, Innovation and Transparency) into action. The following is the final paragraph from 2016 report.

"We are aware that our approach may sometimes cause disruption in the financial sectors that are often dominated by traditional business approaches and mores on how investors should be treated – if it means these disruptive changes we are introducing are pro-client, we will continue to remain steadfast in achieving this outcome in the markets we operate in. When changes are pro-client, we are confident we will succeed in the longer term despite shorter-term challenges."

And I do not think it's just talk. Fundsupermart.com in 2000, FSM Mobile in 2011, Bondsupermart in 2015, and robo-advisor last year are evidences that show that the company is among the first movers.

Crunching the numbersWith the exception of 2016, iFAST has grown both its top and bottom lines, with its EPS growth outpacing its net revenue growth.

Base on the above data, I believe the company should be able to continue to grow its earning at a rate of 20% to 30% for the next few years.

Valuation

Together with the rest of the market, iFAST's price has rebounded quite a bit since the beginning of October and closed at $0.96 on 6 October. Forward PE based on the current price and projected EPS is about 26x. Assuming I am right about its ability to grow at 20% to 30% in the next few years, forward PEG ranges from 1.1 to 1.3. My personal take is that it is fairly priced with potential to surprise on the up side but risk still lingers.

When will I sell?

These four rules still apply.

a. The fundamentals of the company has deteriorate

b. The company is overvalue at the current price

c. To raise cash for a better buying idea

d. To raise cash for other reasons

Conclusion

My first encounter with the company was more than a decade ago when I opened my Fundsupermart account. Did not really use its services as I was on dollardex then. Recently, I wanted to explore its FSMone platform for stock trading and hence decided to register an account. Apparently my record is still in their data base and I need to re-activate my account which I will probably do by the end of the year.

As an investing idea, I came across it somewhere in late 2015 but the PE was crazy then. The sell down due to poor results in 2016 and the recent correction provides me an opportunity to buy a small stake in the company.

I can sense my excitement as I read the development of iFAST over the years and imagine what more can come from them in years to come. Hence, I decided to buy more yesterday at a price of $0.975 (yes, I am not good at market timing). Together with my initial purchases, my average price is $0.93.

I am prepared to add more to this counter at the appropriate junctures.

Friday, 29 September 2017

2017 9M performance

Performance

Another quarter has passed and it's time to take stock of portfolio's performance.

Another quarter has passed and it's time to take stock of portfolio's performance.

It is a muted performance for the quarter, resulting in a slight increase in NAV compared to 20171H performance. In fact, if not for the strong performance of Valuetronics and UMS over the past few days, this quarter will post a return lower than 20171H.

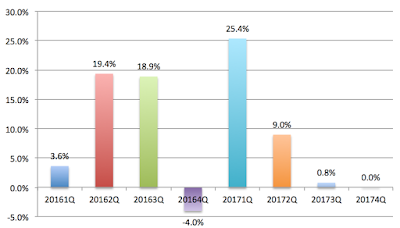

NAV of portfolio grew from $3.78 (30 Dec 2016) to $5.22 (30 Sep 2017), providing a return of 37.8% for 9 months. Definitely happy as this is well above my stretched target of 12% and also beats benchmark STI ETF which returned about 14% (inclusive of dividend) over the same period.

The chart below shows the performance of past 7 quarters.

The muted quarter's performance can be attributed to the following:

- weaker market sentiment for the past quarter,

- continued sell-down of Raffles Medical Group,

- correction of Food Empire,

- divestment of Micro-Mechanics which shot up 20% after I sold, *ouch*

- increase in trading activities as I look for new ideas for the next few years.

Gainers and losers

The following tables show the top gainers and losers for this year thus far. The list should remain pretty much the same by end of the year.

I am glad that 7 out of my 10 core holdings have returned more than 10% thus far this year. Even with the divestment of Best World and Micro-Mechanics, the ratio of 5 out of 8 still looks good.

Looking at the table, it seems that I have a tendency to divest my non-core holding once it has done well. This is something which I wasn't aware of before this post. It will be something that I will take note of in future. Instead of divesting the counter after a strong performance, another option would be for me to spend more effort in understanding the counter and determine the possibility of turing it that into a core holding.

Punting on counters based on minimal information and uncertain business outlook continues to be a game of chance. Fu Yu went 10% up but Oceanus and Innotek went the other way. Not in a hurry to divest Oceanus and Innotek yet as amount put in was minimal, especially for Oceanus. Also, am still feeling positive of a possible turnaround next year or the year after next.

The table also highlighted the strong performance of my three counters in my CPF portfolio which returned 16% thus far. If this continues for the rest of the year, it will be the 9th consecutive year that my CPF portfolio beats STI ETF.

The following tables show the top gainers and losers for this year thus far. The list should remain pretty much the same by end of the year.

I am glad that 7 out of my 10 core holdings have returned more than 10% thus far this year. Even with the divestment of Best World and Micro-Mechanics, the ratio of 5 out of 8 still looks good.

Looking at the table, it seems that I have a tendency to divest my non-core holding once it has done well. This is something which I wasn't aware of before this post. It will be something that I will take note of in future. Instead of divesting the counter after a strong performance, another option would be for me to spend more effort in understanding the counter and determine the possibility of turing it that into a core holding.

Punting on counters based on minimal information and uncertain business outlook continues to be a game of chance. Fu Yu went 10% up but Oceanus and Innotek went the other way. Not in a hurry to divest Oceanus and Innotek yet as amount put in was minimal, especially for Oceanus. Also, am still feeling positive of a possible turnaround next year or the year after next.

The table also highlighted the strong performance of my three counters in my CPF portfolio which returned 16% thus far. If this continues for the rest of the year, it will be the 9th consecutive year that my CPF portfolio beats STI ETF.

Allocation

Dividend vs Growth

With the divestment of two core holdings and exploration of the US market, the allocation looked quite different from the the first half of the year. Cash stands at a high of 15%. Dividend yield of portfolio based on cost is at a low of 3.4%.

With the divestment of two core holdings and exploration of the US market, the allocation looked quite different from the the first half of the year. Cash stands at a high of 15%. Dividend yield of portfolio based on cost is at a low of 3.4%.

Planned

|

Actual

| |

Dividend

|

~ 60%

|

55%

|

REIT/ Business Trust

|

<= 30%

|

25%

|

Growth

|

~ 40%

|

30%

|

Punt

|

<=10%

|

3%

|

Cash

|

0%

|

15%

|

Singapore vs US

Being new to US market, I decided to allocated at most 15% of my fund to it till end of 2018. Currently, it stands at about 12% with 4% invested and 8% in cash.

Action

For the month of September, I have sold

- Dairy Farm at US$8.03 for a gain of 5.0%.

- Singapore O&G at $0.49 for a gain of 2.1%.

- mm2 Asia at $0.49 for a gain of 1.9%.

- Mapletree GCC Trust at $1.15 for a gain of 4.9%.

I have bought the first 3 in August due to their steep drop. Decided to divest them for a quick profit and re-invest them in other counters which I am more familiar with. As for Mapletree GCC, bought it last month with an incorrect understanding of the location of its HK property. Got lucky with it, so decided to take profit.

On the US Market, I have also sold

Dug into the numbers and checked the PE and growth rate of my US counters. The current PE for the first 3 stocks are all much higher than its historical average and PEG are all above 2. Hence, decided to divest them. As for Chiptole, there is currently too much uncertainty and so decided to stay away from it for the moment.On the US Market, I have also sold

- Cognex at US$114.45 for a gain of 3.4%.

- Mastercard at US$140.23 for a gain of 6.1%.

- Priceline at US$1840.60 resulting in a loss of 5.1%.

- Chipotle at US$307 resulting in a loss of 13.4%.

I have added

- more Straco at $0.87. Continue to like its cash generating business. This article by the "Rock" in NextInsight provides a good reading.

- more Hong Kong Land at US$7.28. Same reason as initial purchase in August. Cheap P/B and good results.

- more 800 Super at $1.085 as it continued to trend lower after its announcement of its Q4 results. Two quarters of weaker performances but it has continued to increase its dividend. Looking for a better performance in 2018.

- more Japan Food at $0.435. Same reason as initial purchase - consistent dividend.

- iFAST at $0.87. Its price has slid from its high after announcing a strong 1H results. While its China business will take some time to break even, its other countries performance is growing very well.

- Hock Lian Seng at $0.445. High visibility due to strong record book. If the company is able to maintain its dividend of 2.5 cents, then the yield is about 5.6%.

- ComfortDelgro at $1.995. Bought a tiny stake as I felt that it is oversold. While Taxi business is under great pressure, rail and bus are still doing well. Due to a sudden turn in its share price, I sold it today at $2.08 for a small gain of 2.8%.

Core holdings

Core holdings are counters which I am more familiar with. These are counters which I am more confident of and have a more substantial holding (at least 5% of portfolio); hence I am more likely to hold them for a longer period of time.

The current average holding period is about 2.4 years, as compared to 0.5 years for the remaining holding.

Divestment of Best World and Micro-Mechanics and purchase of VICOM has resulted in partial change of core holdings. These 8 (out of 26) holdings make up 53% of my outlay cost.

The current average holding period is about 2.4 years, as compared to 0.5 years for the remaining holding.

Divestment of Best World and Micro-Mechanics and purchase of VICOM has resulted in partial change of core holdings. These 8 (out of 26) holdings make up 53% of my outlay cost.

- Food Empire (9%) @ $0.46

- Raffles Medical (8%) @ $1.41

- Straco (8%) @ $0.85

- Parkwaylife REIT (6%) @ $2.32

- Valuetronics (6%) @ $0.54

- Fraser Centrepoint Trust (6%) @ $2.03

- VICOM (5%) @ $5.75

- Starhill Global (5%) @ $0.70

Looking Ahead

For the remaining quarter, I am looking forward to dividend from various REITs, 800 Super, RMG, SingTel, UMS, iFast and Japan Food. I am also hopeful of good quarterly result from Food Empire, Straco and Valuetronics which might have a positive impact on their prices. Raffles Medical Group should report another quarter of muted performance.

Barring any unforeseen circumstances, return for the year should be above 35%. With some luck, it might breach the 40% mark.

Monday, 28 August 2017

Buy and sell actions in August

Lots of action this month. Divested a few counters but bought quite a bit with the $$$ from divestment of Best World.

Out of Favour

Divested Kingsmen Creatives at the same price I bought. This is the turnaround story that is not working out yet. It reported a poor Q2 and I decided to wait for a clearer picture before re-entering again.

Divested half my stake in ISEC at 0.315. Tiny profit. Still an interesting outfit but its growth isn't exciting enough for it to occupy the middle of my portfolio. Hence decided to hold less and watch how the story unfolds.

Sold Capital Mall Trust at 2.10. It has risen more than 10% from my purchased price. Covered 2 years of dividend. Will recycle cash to other counters that offer higher dividend yield. Might re-enter when it offers a better yield.

Sold Mircro-mechanics at 1.41. Bought purely for its track record for dividend but its price has gone up to 7 years of dividend due to its good performance. Decided to divest it as its dividend yield dropped below 5%. Surprised me with a second rise of dividend this year and with a 8 cents dividend, yield gone up to 5.6%. On hind side, should have continued to hold on to it but actually felt pretty neutral about it. Probably am satisfied with the above expectation return from the counter.

Up the Dividend

Bought a lot more counters especially REIT to increase my annual dividend. Also, I like their outlook from next year onward.

Added Fraser Centrepoint Trust at 2.07. With the AEI of North Point completing this year, next year DPU should increase. Assuming a 12 cents DPU next year, it will translate to 5.8% yield and potential upside if DPU is even higher. Possible catalyst could be acquisition of Punggol Waterway Point.

Added Starhill Global Reit at 0.76. While Orchard office occupancy could still pose a problem, AEI at Plaze Arcade in Australia is expected to be completed in 20181Q. China property would have a more stable distribution with the completion of renovation by 20174Q. Expecting a minimal 4.8 cents DPU next year. This translates to a 6.3% yield.

Bought CDL Hospitality Trust at 1.575. I have bought and sold CDLHT a couple of times for the past 4 years. Win some, lose some and overall still negative. Betting on the improvement of its hotels in the next two years. Assuming a 10 cents DPU, dividend yield is approximately 6.3%.

Bought Mapletree Commercial Trust at 1.55. A retail and office reit which I have missed for the longest time. Its DPU has been increasing since its listing. Estimating a 9 cents DPU which will give a 5.8% yield.

Bought VICOM at 5.81 (cd) and 5.65 (xd). A subdue Q2 results but with immediate effect it is paying out at least 90% of its earning as dividend. It gives more certainty that the company can maintain its dividend for the next two to three years even when revenue dropped due to increasing de-registration of cars. From 2020/21 onwards, it should see an increase in its revenue and income again with more vehicles requiring checking.

Buying into the Sell-down

Quite a number of counters were sold down for the past month, for good or questionable reasons. The sell-down provided me an opportunity to buy some shares of the counter which I think could do well in the future.

Bought Dairy Farm at USD7.45. The company has announced a decent Q2 recently and turnaround seems to gathering speed with good progress in China. The price was beaten down by 2% to 3% in one of the trading day and I deem it as an opportunity to add some.

Bought InnoTek at 0.34. The stock is beaten down because it reported a poor Q2. However, 1H is still an improvement. While the remaining year might remain a challenge, effort has been put in by management to turn the company around. Initiated the position with the belief that the turnaround will come in 2018 or 2019.

Bought mm2 Asia at 0.475. The price has dropped sharply after its GV deal did not get through. Nevertheless, it reported a good 1Q results and I decided to take a punt on it.

Bought HKLand at USD 7.46. Read about its cheap P/B and good results. Hence, decided to take a stake when its price has dropped by about 5% from its recent high.

Bought UMS at 0.995. The price has dropped sharply after guidance of moderate performance in 2H. Nimble a bit as I believe it will maintain its dividend which is a tasty 6%.

Bought 800 Super at 1.12. The price has dropped after a poor Q3. The price weakened further just before it announced its full year results. Took the opportunity to re-enter the counter which I have divested at 1.26 in April.

Bought Singapore O&G at 0.44. The price has dropped sharply after its weak Q2 results. Took a punt on it as company is still profitable and should get better results moving forward.

US Market

Most of my purchase decision for the US markets come from the recommendation of MF subscription services. Unlike my local counters, I did not do as much homework on them. While I think that the valuations of the counters are high, I like their future stories hence my stake in them. All my purchases are small and will slowly wait for opportunity to accumulate more shares in the future.

Bought Vail Resort at USD210.51. Luxury ski resorts operator. It has been growing through acquisition and opportunities to grow is still available. Its plan to keep its resort busy all-year round is working out well with Epic Discovery activities coming on more than one location.

Bought Cognex at USD105. Machine-Vision systems are used all around the world. Growth expected to continue.

Bought Priceline at USD1870. Good Q2 results but market is spooked by its lower Q3 guidance. Taking this opportunity to have one bite on it.

Bought Intuitive Surgical at USD935. Intuitive Surgical have been growing for many years and its recurring income has increased. Decided to buy 2 shares to participate in its growth even though it has a high PE of 44x.

Out of Favour

Divested Kingsmen Creatives at the same price I bought. This is the turnaround story that is not working out yet. It reported a poor Q2 and I decided to wait for a clearer picture before re-entering again.

Divested half my stake in ISEC at 0.315. Tiny profit. Still an interesting outfit but its growth isn't exciting enough for it to occupy the middle of my portfolio. Hence decided to hold less and watch how the story unfolds.

Sold Capital Mall Trust at 2.10. It has risen more than 10% from my purchased price. Covered 2 years of dividend. Will recycle cash to other counters that offer higher dividend yield. Might re-enter when it offers a better yield.

Sold Mircro-mechanics at 1.41. Bought purely for its track record for dividend but its price has gone up to 7 years of dividend due to its good performance. Decided to divest it as its dividend yield dropped below 5%. Surprised me with a second rise of dividend this year and with a 8 cents dividend, yield gone up to 5.6%. On hind side, should have continued to hold on to it but actually felt pretty neutral about it. Probably am satisfied with the above expectation return from the counter.

Up the Dividend

Bought a lot more counters especially REIT to increase my annual dividend. Also, I like their outlook from next year onward.

Added Fraser Centrepoint Trust at 2.07. With the AEI of North Point completing this year, next year DPU should increase. Assuming a 12 cents DPU next year, it will translate to 5.8% yield and potential upside if DPU is even higher. Possible catalyst could be acquisition of Punggol Waterway Point.

Added Starhill Global Reit at 0.76. While Orchard office occupancy could still pose a problem, AEI at Plaze Arcade in Australia is expected to be completed in 20181Q. China property would have a more stable distribution with the completion of renovation by 20174Q. Expecting a minimal 4.8 cents DPU next year. This translates to a 6.3% yield.

Bought CDL Hospitality Trust at 1.575. I have bought and sold CDLHT a couple of times for the past 4 years. Win some, lose some and overall still negative. Betting on the improvement of its hotels in the next two years. Assuming a 10 cents DPU, dividend yield is approximately 6.3%.

Bought Mapletree Commercial Trust at 1.55. A retail and office reit which I have missed for the longest time. Its DPU has been increasing since its listing. Estimating a 9 cents DPU which will give a 5.8% yield.

Bought VICOM at 5.81 (cd) and 5.65 (xd). A subdue Q2 results but with immediate effect it is paying out at least 90% of its earning as dividend. It gives more certainty that the company can maintain its dividend for the next two to three years even when revenue dropped due to increasing de-registration of cars. From 2020/21 onwards, it should see an increase in its revenue and income again with more vehicles requiring checking.

Buying into the Sell-down

Quite a number of counters were sold down for the past month, for good or questionable reasons. The sell-down provided me an opportunity to buy some shares of the counter which I think could do well in the future.

Bought Dairy Farm at USD7.45. The company has announced a decent Q2 recently and turnaround seems to gathering speed with good progress in China. The price was beaten down by 2% to 3% in one of the trading day and I deem it as an opportunity to add some.

Bought InnoTek at 0.34. The stock is beaten down because it reported a poor Q2. However, 1H is still an improvement. While the remaining year might remain a challenge, effort has been put in by management to turn the company around. Initiated the position with the belief that the turnaround will come in 2018 or 2019.

Bought mm2 Asia at 0.475. The price has dropped sharply after its GV deal did not get through. Nevertheless, it reported a good 1Q results and I decided to take a punt on it.

Bought HKLand at USD 7.46. Read about its cheap P/B and good results. Hence, decided to take a stake when its price has dropped by about 5% from its recent high.

Bought UMS at 0.995. The price has dropped sharply after guidance of moderate performance in 2H. Nimble a bit as I believe it will maintain its dividend which is a tasty 6%.

Bought 800 Super at 1.12. The price has dropped after a poor Q3. The price weakened further just before it announced its full year results. Took the opportunity to re-enter the counter which I have divested at 1.26 in April.

Bought Singapore O&G at 0.44. The price has dropped sharply after its weak Q2 results. Took a punt on it as company is still profitable and should get better results moving forward.

US Market

Most of my purchase decision for the US markets come from the recommendation of MF subscription services. Unlike my local counters, I did not do as much homework on them. While I think that the valuations of the counters are high, I like their future stories hence my stake in them. All my purchases are small and will slowly wait for opportunity to accumulate more shares in the future.

Bought Vail Resort at USD210.51. Luxury ski resorts operator. It has been growing through acquisition and opportunities to grow is still available. Its plan to keep its resort busy all-year round is working out well with Epic Discovery activities coming on more than one location.

Bought Cognex at USD105. Machine-Vision systems are used all around the world. Growth expected to continue.

Bought Priceline at USD1870. Good Q2 results but market is spooked by its lower Q3 guidance. Taking this opportunity to have one bite on it.

Bought Intuitive Surgical at USD935. Intuitive Surgical have been growing for many years and its recurring income has increased. Decided to buy 2 shares to participate in its growth even though it has a high PE of 44x.

Sunday, 12 February 2017

January and February Portfolio

It has been a busy past 6 weeks. Things are finally looking to settle a bit and it's time to continue to keep in touch with my thinking and reflection on my investment.

It has been a good start to the year for the market and my portfolio also benefitted from it. Year to date, it has returned 12.8%. Woohoo, I hit my target in less than two months. So would I achieve another 40% return this year? I hope so but you never know. Who knows? The market might just turn south any time. So continue to monitor the company's performance and invest/divest at the right time for the long term.

I have divested the following for the first one and a half month to increase my cash buffer and to reduce my REIT exposure.

It has been a good start to the year for the market and my portfolio also benefitted from it. Year to date, it has returned 12.8%. Woohoo, I hit my target in less than two months. So would I achieve another 40% return this year? I hope so but you never know. Who knows? The market might just turn south any time. So continue to monitor the company's performance and invest/divest at the right time for the long term.

I have divested the following for the first one and a half month to increase my cash buffer and to reduce my REIT exposure.

- Best World: Partial sold as it has rose more than 50% within a month. It continue to be in my top 5 stocks holding.

- Thai Beverages: Among the few counters that I punted, I am just more excited about the rest.

- Raffles Medical Group: Partial sold to reduce my exposure. Remain my top stock in terms of initial capital outlay.

- CDLHT: To reduce my REIT exposure to within 30%.

- Starhill Global: To reduce my exposure to retail reit. And currently I favour neighbourhood reit more.

I have added the following positions.

- Valuetronics: Increased my stake slightly for its dividend.

- UMS: Bought a small stake after reading its plan to divest its customer base and attracted by its consistent dividend.

- Micro-mechanics: Increased my stake after it announced its good improvement in its latest quarter. Attractive dividend and potential of further growth.

- Dutech: Took a very small stake after reading Thumbtack Investor's detailed analysis

- Sing Medical: Took a very small stake as I perceived that the new management will continue to improve the group's performance

- Fraser Logistics and Industrial Trust: Took a very small stake after reading about it on The Edge and Dividend Warrior's analysis.

After the above actions, my top 5 holdings in terms of initial capital outlay are:

- RMG @ average price of $1.48

- Plife Reit @ average price of $2.32

- Straco @ average price of $0.84

- BWL @ average price of $0.60

- FCT @ average price of $2.01

Subscribe to:

Posts (Atom)